INTRODUCTION

Anyone with a job or some kind of regular income has a great chance to build wealth over the long term if they are prudent enough. To be able to do this they just need to be a little bit financially literate. The trick is to maximize your earnings while optimizing your spending. The gap between your wages and expenses becomes your investment capital which you can then allocate to your investments. You don’t need a lot of cash to start investing. All you need is ugx 100,000. Investing is like any other skill. You get better with practice and experience and lots of mistakes.

KEY CONSIDERATIONS

While thinking of where and how to invest your money the following key considerations have to be made:

a) What are your Money Goals and Objectives?

b) How much funds are available for investment?

c) What is your risk profile?

d) What is the expected return of investments?

e) How long should you invest for?

f) Do you have the skills/time/experience/energy to manage the investments?

g) What is your investment strategy?

Depending on the answers to these question there are various investment options available to an individual.

POSSIBLE INVESTMENT OPTIONS

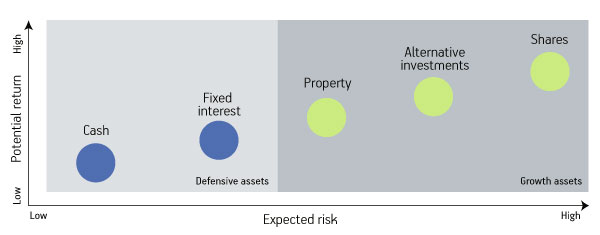

Investments fall into two broad asset classes – growth and defensive. Growth assets are designed to grow your investment. They include investments such as shares, alternative investments and property. They tend to carry higher levels of risk, yet have the potential to deliver higher returns over longer investment time frames. Defensive assets include investments such as cash and fixed interest. They tend to carry lower risk levels and, therefore, are more likely to generate lower levels of return over the long term. Generally, defensive assets are expected to provide returns in the form of income and give you some peace of mind. They also give you liquidity. The main consideration is to balance liquidity with growth. You need to have enough cash to survive but also invest enough cash to grow your wealth.

Depending on the risk/return relationship for each asset class we can broadly categorise investments into defensive assets and growth assets as shown in Figure 1.

Figure 1: Asset risk and return characteristics

INVESTMENT/ASSET CLASS CHARACTERISTICS

This section highlights some of the characteristics of the most common investment options available to an individual. The list is in no way exhaustive but can give you a feel of what is available.

GROWTH ASSETS

SHARES

Shares are securities that represent ownership in a listed company. To invest on the Uganda Securities Exchange you need to open up an SCD account with a broker. Returns come from increases or decreases in value. Returns also come from income from the company’s profits which are paid to shareholders as dividends. Shares potentially earn the highest return over the long term. However the value is more likely to fluctuate in the short term. Shares are generally considered a high-risk investment. The minimum amount required to buy shares is only ugx 100,000.

BUSINESS

There are many businesses to choose from e.g. schools, shops, agribusiness, trade and retail, manufacturing, farming, professional services, etc. Returns from business come from increases or decreases in value of your shareholding/investment. Returns also come from income from the company’s profits which are paid to shareholders as dividends. Businesses can potentially earn more than property, fixed interest and cash over the long term. The business asset value tends to fluctuate more than property, fixed interest and cash in the short term. They are generally considered a medium-to-high risk investment. You need to have a reliable team to manage the business on your behalf if you’re still employed full time. The capital requirement for business really depend on the nature and scale of business. You can start a side hustle selling second hand shoes with only ugx 100,000.

PROPERTY

Property may include industrial, retail or commercial real estate including land. Returns come from increases or decreases in value. Returns also come from income in the form of rent in case of rentals. Property investments potentially earn more than fixed interest and cash over the long term. The value tends to fluctuate more than fixed interest and cash but not shares, over time. They are however not easily converted to cash. Property can be used as collateral to access financing from banks. The capital requirements for business depend on the location, size and nature of property. You can buy a plot of land in Zirobwe for ugx 3m. You can buy an acre of farmland in Nakasongola for ugx 3m.

DEFENSIVE ASSETS

CASH

This asset class includes money in bank deposits (savings + fixed deposits), money in short-term money market securities, and collective investment schemes (Unit trusts). Returns come from interest paid on the amount invested. Returns also come from increases or decreases in value of the underlying securities due to changing interest rates. The chance of losing money on a cash investment considered remote over a one-year period, but possible. Cash is generally a stable investment that provides steady returns. The value tends to fluctuate due to changing interest rates. The minimum amount required to participate in unit trusts is only ugx 100,000.

FIXED INTEREST

Fixed interest assets include: Treasury Bonds and Bills; and debentures (Loans to Companies). The returns come from interest paid on the loan amount. (When buying fixed-interest securities, investors are ‘loaning’ money to a corporation or government at an interest rate.) Returns also come from increases or decreases in value of the underlying securities due to changing interest rates. These assets tend to provide better returns than cash over the long term, but lower returns than property and shares. The value tends to fluctuate more than cash but less than property and shares. The minimum amount required to participate in treasury bills is only ugx 100,000.

BASIC ASSET ALLOCATION STRATEGIES

You want to have a fair balance between growth and defensive assets. Growth assets give you potential to grow your wealth quickly though they carry a bit of risk. Defensive assets give you peace of mind and liquidity. I would advise that you start with defensive assets at the beginning of your career and then diversify as you move up. Start by investing in simple things like units trusts, fixed deposits, treasury bills, etc. Then move up to land, etc. You can also experiment with shares at this point. If you can, invest in your residential home to get some safety before gambling with risky investments. Thereafter try your hand at business and larger projects with higher risk profiles. Remember, investing is like any other skill. You get better with practice and experience and lots of mistakes.

Great Article.

Thanks

LikeLike